Evgen verzun

Blog

All cybersecurity articles

All cybersecurity articlesMarch 23, 2023

Banking Crisis at Center Stage: Who Are The Biggest Winners and Losers?

In the past few weeks we’ve witnessed a certified banking collapso-palooza - three US banks went belly up, causing a ripple effect on the entire traditional banking sector.

First off, let’s look at the downfall of the Silicon Valley Bank (later SVB), the former 16th-largest bank in the United States. After being given a clean bill of health just in February, the state-chartered commercial bank ‘inexplicably collapsed’ after 40 years of stability. How come?

If we were forced to pin down the cause of SVB’s death in one sentence, we could simply say ‘they fell victim to a typical bank run, poor risk management and unfavorable market conditions’.

But! The situation is more complex than it meets the eye.

What Led To SVB’s Insolvency?

Let’s kick off with a fun fact.

Banks have a reserve requirement, the amount of cash that financial institutions must have in their vaults or at the closest Federal Reserve bank, in line with deposits made by their customers.

It can wary wildly, but for the sake of simplicity, suppose we have a 10% reserve requirement, meaning that a bank that has 100 million dollars really only has to have 10 million dollars in their coffers at all times. All the remaining money is out there, multiplying itself in the wild and enriching the economy we rely on.

Kinda scary, right? But it kind of works. In a world where all people trust the system and feel that their deposit is safe. But… this is not the world we live in right now. When people freak out all at once, banks sometimes crumble, SVB being one such example.

But how exactly did SVB get there?

- Despite being a massive lender to US tech startups crypto companies, SVB was not investing its customers money in crypto, instead picking up long duration US treasury bonds at a low interest rate. They thought they played it safe!

- The Federal Reserve decides to battle inflation by introducing aggressive interest rates. Banks holding government bonds suddenly find their assets are worth less than they expected. And while the bigger fish could swallow this bait just fine, it isn’t the case for smaller institutions. While not ideal, this is still not the end of the world for SVB.

- Here’s a kicker… SVB customers are startups who have a hard time raising capital, now more than ever. See where this is going? SVB doesn't have enough money coming in the door, it’s red alert time.

- Now they have to get money somehow, somewhere. That’s when they decide to bite the bullet and sell those bonds at a near $2 billion loss. Since that is still not enough, SVB goes out of their way to ask for more money from other banks. It doesn’t look good.

- Customers watch the news, talk to each other, and freak out. Something that banks can’t deal with happens - businesses rush to pull their money out, since they are not insured by the government. Bank run is in full force now!

- SVB stocks tumble down, and the bank has even more problems raising capital. “Hey, aren’t you that bank that we have seen in the news? Sorry, can’t help you. But they can!”

- Federal regulators knock on the door and say they will take it from here. Fin.

And that’s how it ended for Silicon Valley Bank. Of course, the downfall of SVB alone wouldn’t be enough for a full fledged banking crisis that would be compared to 2008 by some, so more trouble follows.

When It Rains, It Pours…

As they say, bad things come in threes!

Silvergate, a crypto friendly bank that suffered heavily after the bankruptcy of FTX announces plans to wind down and liquidate. With SVB and Silvergate down for the count, worries of bank runs spread through the masses even more, and balance sheets simply aren't robust enough to deal with depositors taking their money out. It’s bad news all around.

Regulators hold some emergency meetings, then take control of Signature Bank, who are additionally investigated for failing to properly scrutinize clients' activities for signs of money laundering. The situation grows to international proportions and Credit Suisse Group, a global investment bank and financial services firm founded and based in Switzerland ‘joins the party’,

They also had missteps over risk management going back years, a fair share of loud scandals, money laundering schemes, heavy losses - the whole nine yards.

CSG’s shares hit a new low, and so they borrowed up to 50 billion Swiss francs from the Swiss central bank to shore up its liquidity. Didn’t help though. Despite the lifeline from the Swiss central bank, things still go western, and UBS Group takes over, as a part of an urgent effort by Swiss and global authorities to ‘restore trust in the banking system’.

The effort was urgent alright, but was it effective? Do people feel confident enough in the opaque banking system? Can they resist the urge to move deposits with a click of the mouse? Nope.

While The Banks Were Imploding, Retail Bought

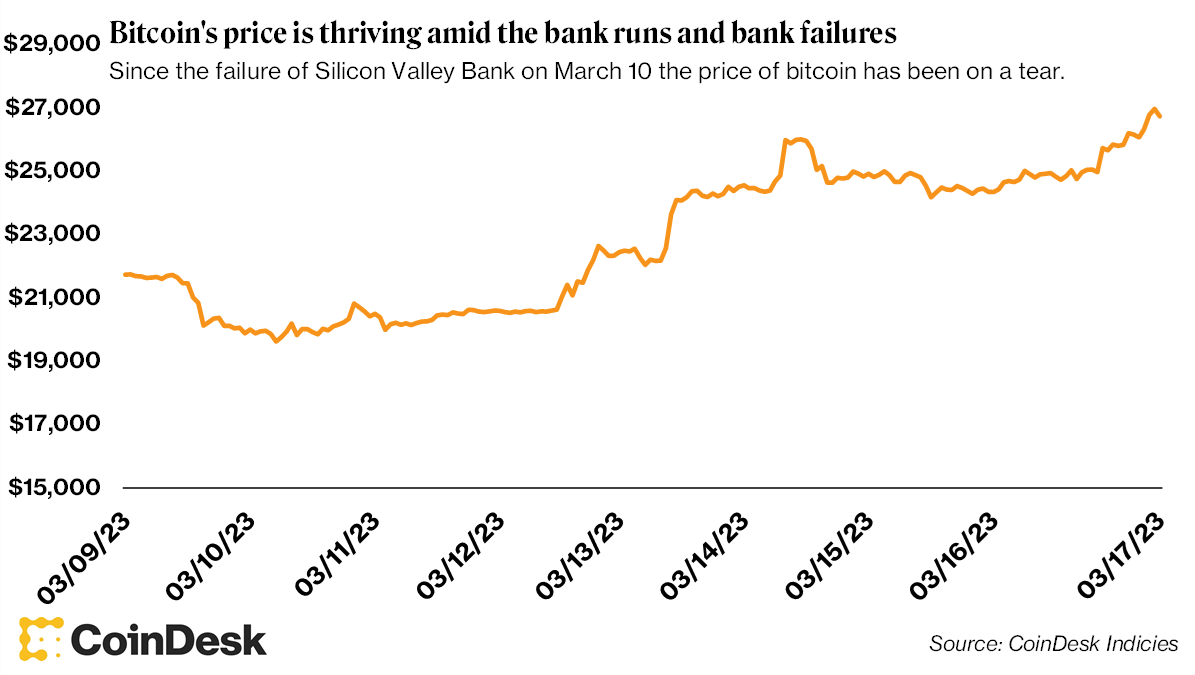

"This Is Good For Bitcoin" is an ironic catchphrase used online to describe how issues we encounter make Bitcoin a bit stronger. All jokes aside, the banking crisis benefitted the king of cryptos, and this banking chaos was very good for Bitcoin.

Bitcoin climbed past the $28,000 level as investors rediscover its appeal as an alternative banking system. Bitcoin is often referred to as “digital gold”, a store of value, particularly in moments of global turmoil. This is why it has been created in the first place - to be an alternative to the current financial system, which often shows signs of weakness when things don’t go well.

It is coming off its best week since January 2021, which was right before the bull run.

But I hear some of you asking, didn’t some of those banks go under because they were to deep in crypto, which took a nosedive in the past year? Not really.

These banks aren’t in trouble because of bets on crypto or the companies in those industries. Instead, fractional reserve banking system is under stress due to the raising of rates by a multiple of almost 20 over the last year. Сrypto is seen as a redheaded stepchild sometimes, but it had little to do with the collapse of all those banks.

The system is showing cracks, banks fail, people buy BTC, driving its price up.

The recent slump of USDC showed us exactly why stablecoins need banks to be stable, but Bitcoin, with its fixed issuance at a time of monetary expansion, looks like a way to opt out of this most recent crisis.

“I Hate To Say That I Told You So, But I Told You So”

There’s a portion of people who have lost hope in the financial system some time ago.

Even though crypto executives and investors had a rough year themselves, the news about the banking crisis provided them with a good opportunity to remind everyone about how they're actually in the right all along. Myself included!

Let’s go only through those positives that make sense in this context:

- Decentralization: Cryptocurrencies are decentralized, they are not controlled by any single entity or government. This is an advantage over traditional financial systems, which are often vulnerable to corruption, mismanagement, and panic.

- Transparency: Blockchain technology provides a transparent and immutable record of all transactions. This transparency helps build trust in the ecosystem, as it ensures that all transactions are verified and cannot be altered retroactively.

- Accessibility: Crypto can be bought and sold online, which makes them accessible to anyone with an internet connection. This can be especially beneficial for people in countries with limited access to traditional financial services.

Now look at the first letters of each list item. DTA - don’t trust anybody!

The main idea of crypto is to be your own bank, and while it can sound like a pain in the backside, it can actually be a good idea for some of us.

Here’s a few more reasons why banks aren’t as responsible as you think they are.

- Banks engage in excessive risk-taking by investing in assets or making loans to borrowers who are unlikely to repay. If these investments or loans don’t deliver, the bank faces significant losses. There’s little reason to be sensible with those bets, since most of the time the government will bail out the failing bank to hush down the public fears.

- Banking crises are caused by systemic financial imbalances such as large current account deficits, high debt levels, significant economic disparities between different regions or countries.

- There’s also credit bubbles and asset price inflation. These occur when there’s a rapid increase in the availability of credit, which leads to an increase in the demand for assets such as real estate, stocks, and bonds. As asset prices rise, borrowers may take on more debt than they can afford to repay, and when the bubble bursts, they may default on their loans.

- Inadequate regulatory oversight contributes to banking crises. Banks engage in risky or fraudulent behavior without real repercussions.

- Let’s not forget about external events such as wars, natural disasters, or pandemics. They can also trigger banking crises by disrupting economic activity and leading to defaults on loans.

All these factors reinforce each other and create a vicious cycle most banks are not able to get out of on their own.

Back in 2008 there was a system-wide problem, where banks all around the world suddenly realized that they were exposed to rotten investments in the US housing market. That led to enormous government bailouts and a global economic recession many of us still remember like it was yesterday.

Since then, banks had to hold more capital and follow the rules. But here we are in the year of 2023, and the nervousness around the health of banks is stronger than ever.

People worry about their deposits and have the means to move them fast. Some are not so lucky though…

What About The Startups?

The banking crisis is not the end of the world for regular people, since the government promises to pay back everyone who has less than $250,000 in their account.

But it’s not the case for businesses, who need much more money to chug along. They have rent to pay, cover the payroll, simply do their business. 90% of SVB’s customers, for example, had way more than $250,000 to their name, which in turn triggered the lethal bank run.

Businesses knew they wouldn’t be safe. Some of them moved to First Republic only to find themselves caught up in a bank run again.

They say insanity is doing the same thing over and over again, but expecting different results.

Unfortunately, founders often have no choice. Many startup founders choose a regional bank instead of a larger institution when they first launch the company. If you are a founder with an early-stage company and have no venture capital backing, you have to settle on a smaller bank.

Or… maybe, just maybe, choose to change their approach entirely and turn their heads to decentralized finances. Regulators are trying their best to send a strong anti-crypto message, so one has to wonder, do they feel threatened?

Because it’s really funny how things can work out sometimes!